Trump’s tax on trade: Rationale ranges from raising money for tax cuts to bringing back manufacturing

Editors choice

American consumers love to buy stuff, and they don’t really care where it comes from if the price is right. And American businesses are pretty good at making stuff, and to do that they need metal, chemicals, parts and thousands of other items – and where that comes from matters less than whether the price is right and the supply is dependable.

Add those together and you get a $3 trillion import tab. It’s a massive inflow of goods to the US and outflow of cash overseas that President Donald Trump wants to hit with taxes, known as tariffs, that add to the cost of any inbound product, and he has unveiled a blitz of tariff plans since returning to the White House in January.

Trump’s rationale ranges from raising money to pay for tax cuts to bringing back manufacturing to the US to leveraging concessions from trading partners, and the idea has raised concerns about a global trade war. Rates as high as 25 per cent on goods from Mexico and Canada, for example, are slated to go into effect March 4.

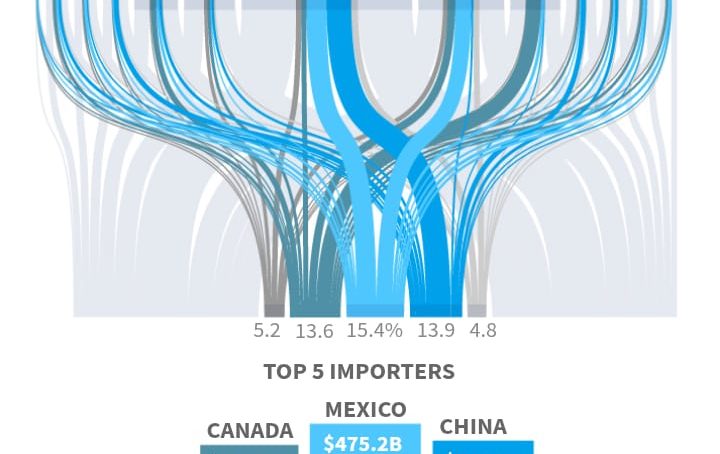

Nearly half of US imports come from three countries: China, Canada and Mexico, now the leading sources of imports. China is considered a geopolitical adversary, but the US has had free trade agreements with Canada and Mexico for decades. Tariffs, though, could become steep for all three.

The range of goods involved is extensive and supply chains are complex. So is the economic impact. China’s manufacturing prowess hollowed out entire US industries but has also helped keep inflation low. And the year-round availability of avocados from Mexico even became a Super Bowl ad meme.

Is past prologue?

In the decades right after World War II, with pent up demand from wartime rationing and a baby boom underway, US factories pumped out the cars to transport a growing population, the food to feed everyone, and the furniture and appliances to fill their homes. Imports were a luxury.

Tariffs were high, but supply networks – all the highways, ports, warehouses and computers needed to shuffle things around and track them – were not as extensively developed as they are today.

Imports, a modest share of economic activity in the 1960s, accelerated as the US began importing things like German and Japanese autos, then took off in earnest in the 1990s under various free trade agreements.

Imports as a share of us GDP

Globalisation, long championed by Republicans before Trump’s “America First” mantra rewrote their narrative, had a noticeable hand in keeping inflation low for years, a benefit to consumers of all means.

The US began opening its markets with tariff cuts in the 1970s. Then, deals like the North American Free Trade Agreement drove them down further in the 1990s, and that process remained intact until Trump’s first term starting in 2017.

Ask a dozen experts about how tariffs effect an economy and you’ll get a dozen different answers. The rates imposed, how widely they are applied, whether trading partners retaliate and just how consumers respond all influence whether manufacturers eat the cost or pass it on through higher prices. Other countries impose their own levies or other restrictions on US goods. Consumers might rebel and buy a cheaper domestic substitute – or decide that avocado is worth it after all. Opinion polls show the public is divided as well.

Partisan politics also colour the response: Democrats have at times been suspicious of globalisation, but in one recent survey they were largely opposed to tariffs. Republicans were more supportive, but lukewarm.

It isn’t just consumer goods like those Mexican avocados or French wines or Bangladeshi T-shirts that are imported. US industries also import vast amounts of equipment, parts and machinery from abroad to power their own factories. Canada, meanwhile, is a major source of energy and raw materials like lumber for homebuilding and potash for agriculture.

In deciding on its final tariff strategy the administration is already facing demands for exemptions. Some goods like autos now have parts and subassemblies that cross the US-Canada or US-Mexico border several times before completion, with value added at each step. Which bits should be taxed and at which rate?

One survey of responses to tariffs had some potentially tough news for the US economy. Consumers seemed ready to stockpile what they could at current prices, shop more carefully, and save more, all of which might point to a slower economy in the future. Business managers, meanwhile, were ready to get picky about supply chains but were also poised to raise prices.

The net influence on the US may not be known for months, after full details of Trump’s plans are rolled out and are put in place. Economists often regard tariffs as a one-off price shock that may not resonate broadly. But a full-on trade war, with responses and counter-responses, could be globally damaging. And the extent of what Trump is suggesting, should it all come to pass, has prompted many analysts, including staff at the US Federal Reserve, to pencil in faster inflation and slower growth, a potential blow to households from two directions.

The dollars and cents impact is one thing. How it affects public psychology poses its own risks. Some consumer surveys have pointed to rising inflation expectations, something that can help push inflation itself higher.

The sweeping nature of Trump’s plans, hitting close trading partners and core industrial goods, has created the sort of uncertainty around the economic outlook that could push down business investment, a further drag on growth. That could, of course, be offset if firms see opportunity to avoid tariffs by moving operations to the US, a dynamic that would only be clear over time.

Uncertainty is part of life, sure. But the Trump years have been exceptional, with uncertainty pushed to record levels even before the COVID-19 pandemic erupted in 2020, near the end of his first term. His return to office has created a similar level of fogginess about what’s next.

In his last term, businesses were buoyed by tax cuts even as the global economy slowed due to a trade war, and domestic investment rose as a share of GDP. Inflation was not an issue, and the US Federal Reserve actually ended up cutting interest rates.

This time may be different.

Inflation remains top of mind, the economy is growing, and the unemployment rate is low, all conditions that might make businesses more likely to pass along tariffs into higher prices, and that might prompt the Federal Reserve to respond if they do.

US Global Imports: US Census data via Fitch Ratings; Imports as a share of GPD, Change in Inflation: US Census Bureau via Federal Reserve Bank of St. Louis; Average Tariffs: US Census data and International Trade Commission data via Tax Policy Institute; Survey via Olivier Coibion, University of Texas at Austin; Yuriy Gorodnichenko, University of California, Berkeley; Michael Weber, University of Chicago, Booth School of Business; Steel and Aluminum Imports: US Census Data from S&P Global Market Intelligence via Department of Commerce; Economic Policy Uncertainty Index: US Census Bureau via Federal Reserve Bank of St Louis

- A Reuters report

About author